The Fraud Hiding in Plain Sight: How Cash Flow Data Catches What Credit Scores Miss

Income manipulation. Loan stacking. Synthetic identities. The signals are there — if you know where to look.

Fraud doesn’t always look like fraud. It rarely shows up as an obvious red flag in someone’s credit file. More often, it looks like a reasonable application from a borrower with a decent credit score, a legitimate-sounding employer, and income figures that check out — on paper.

The problem is that “on paper” is increasingly easy to fake. Income documents can be manipulated. Pay stubs can be generated with a few minutes and a free online tool. Cash flow data changes that. When you can look directly at a borrower’s actual bank transactions, the money either showed up or it didn’t.

The Most Common Fraud Patterns — and What They Look Like in the Data

Income Manipulation

This is the most widespread form of application fraud. A borrower inflates their income on the application — sometimes dramatically. Cash flow underwriting makes this much harder to pull off. When you’re looking at 12–24 months of raw transaction data, irregular, inconsistent, or missing deposits are an immediate signal.

The most dangerous fraud isn’t the obvious kind. It’s a fabricated income that passes a surface-level check. Real bank transaction data is the most reliable way to verify what’s actually happening in someone’s financial life.

Loan Stacking

Loan stacking happens when a borrower applies for multiple loans from different lenders simultaneously — before any of the new debt shows up on their credit file. Cash flow analysis catches the signs: multiple large recent deposits from other financial institutions, unusually high existing debt service payments, or transaction patterns consistent with drawing down new credit lines.

Synthetic Identity Fraud

A synthetic identity is built from real and fabricated information. The fraudster spends months building a credit history for this fictional person before taking out large loans. Synthetic identities can be hard to catch with credit data alone — but cash flow adds a layer of verification. Does the income story match the credit story? Is account activity consistent with the life that credit file suggests?

Gig Income Misrepresentation

Whether intentional or not, a loan sized to income that isn’t there creates real risk. Cash flow underwriting gives lenders an accurate view of actual gig earnings over time, not just a snapshot of an unusually good month.

Why Credit Scores Alone Can’t Solve This

Credit scores are backward-looking by design. The fraud is happening at the application layer, not the credit layer. To catch it, you need data that reflects what’s actually happening right now — transaction-level cash flow data.

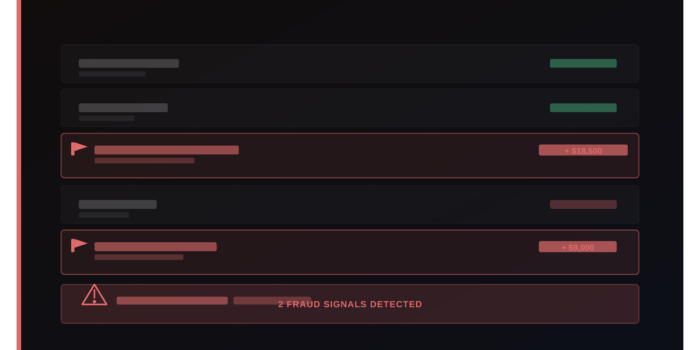

How Kora Surfaces Fraud Signals

Kora’s platform analyzes transaction data across dozens of dimensions: income consistency and source verification, deposit timing and frequency, balance behavior over time, and anomalies suggesting document manipulation. These signals feed into the Kora Score — legitimate borrowers get approved faster, suspicious applications get flagged before the loan is made.

Catch fraud before it costs you.

See how Kora’s platform flags risk signals that credit scores miss.