Cash Flow Underwriting for Credit Unions: The Complete Guide

How credit unions can grow their loan portfolios, serve more members, and reduce risk — all at once.

Credit unions are built on a mission that most banks can’t claim: serving members, not shareholders. That means saying yes to loans that help members build financial stability, not just loans that are easiest to approve. It also means being careful stewards of the capital that belongs to those same members.

Cash flow underwriting sits squarely at the intersection of both goals. It helps credit unions approve more creditworthy members — including the ones who’ve been let down by traditional credit scoring — while maintaining the rigorous risk standards the mission demands. Here’s everything credit union lending teams need to know.

Why Credit Unions Are Uniquely Positioned for Cash Flow Underwriting

Credit unions already have something most other lenders don’t: deep relationships with their members. Many credit union members have their primary checking and savings accounts at the institution. That transaction data — the income, spending, and savings behavior playing out in real time — is potentially sitting right there.

Cash flow underwriting turns that existing relationship data into a lending advantage. Instead of relying solely on a credit score that may not reflect your member’s current financial reality, you can look at what’s actually happening in their account. It’s a more complete picture — and for credit unions committed to serving members fairly, it’s a more equitable one.

The Members Credit Unions Are Currently Missing

Low-to-Moderate Income Members

Members with thin credit files or subprime scores who manage their money responsibly but simply haven’t accumulated significant credit history. These are exactly the members a community-focused credit union exists to serve — and cash flow data reveals the borrowers among them who are strong credit risks.

Young Members

First-time borrowers in their 20s who are just starting their financial lives. They may have limited credit history, but their transaction data tells a real story about income stability and financial habits that a credit score simply can’t tell yet.

Self-Employed and Gig Worker Members

Independent workers, small business owners, and gig economy participants whose income doesn’t fit neatly into a W-2 box. Their earnings may be strong and consistent, but traditional underwriting models are poorly equipped to evaluate them.

Credit unions exist to serve members that larger banks overlook. Cash flow underwriting gives credit union lending teams the tools to do that responsibly — approving more members without taking on more risk.

How Cash Flow Underwriting Works in a Credit Union Context

When a member applies for a loan, they consent to sharing their bank account data — including accounts at other institutions if their primary account isn’t with you. That data is analyzed to produce a detailed picture of their financial health: income sources and consistency, spending patterns, existing debt obligations, cash reserves, and any signals of elevated risk.

For credit unions using Kora, all of that analysis flows into the Kora Score — a single, consistent metric that integrates directly into your loan origination system. Your underwriting team sees the score, the supporting detail, and any risk flags, all within the workflow they already use. No process overhaul required.

The Compliance Picture

Fair lending compliance is a top priority for credit union lending teams. Cash flow underwriting, when implemented correctly, actually supports fair lending objectives — it allows you to approve members from underserved communities who would be declined under a credit-score-only model, which is precisely what fair lending regulations are designed to encourage.

Kora’s platform generates FCRA-compliant adverse action codes alongside every score, so your team can clearly communicate decisions to members and satisfy regulatory requirements.

What Credit Unions Actually See After Implementation

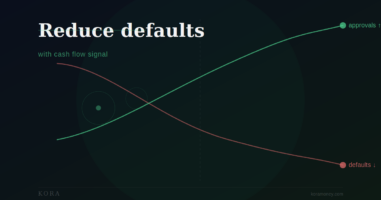

Credit unions that implement cash flow underwriting typically see three things: approval rates increase for members who were previously declined despite being strong credit risks; default rates hold steady or improve because additional data improves risk accuracy; and member satisfaction improves because more members get the financial support they came to their credit union to find.

More approvals. No more defaults. Happier members. That’s the credit union mission in practice.

Ready to serve more members responsibly?

See how Kora’s cash flow underwriting platform is built for credit unions.